Business Clients

From tax efficiency today through to planning a comfortable retirement tomorrow, we help you manage your corporate and personal finances wisely throughout the life of your business, while shielding you against unforeseen problems that can threaten its success.

Crystal Wealth Management is a team of truly independent financial professionals, offering you the full range of financial planning and management services. We gain a thorough understanding of your business and your aspirations, becoming a trusted advice hub and proactively keeping you informed of changes and opportunities. Put simply, we’ll help you to set and achieve your financial objectives while giving you the freedom and peace of mind to concentrate on running your business. Services and Business AdviceOur services and advice for business cover many considerations.

1. Tax Mitigation

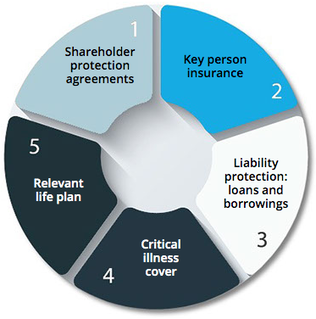

All business owners aim to increase turnover and profits but most also wish to minimise their tax liabilities: after all, it’s not just what you earn that matters, it’s what you keep that counts! As corporate planning professionals we analyse the tax mitigation opportunities appropriate for your business, advising on beneficial strategies to reduce corporate and personal tax liability including Corporation Tax, Income Tax and Capital Gains Tax. Additionally, we advise on corporate trust planning and tax-efficient staff remuneration. Please note, tax planning is not regulated by the Financial Conduct Authority. 2. Company Investments, Savings and Loans Benefit from an objective review of your savings and borrowings, including the efficiency of your financial structure, cash management strategies and existing pension policies. We can usually find ways to save you money and reduce your tax liabilities. 3. Business protection: Safeguarding your business and its beneficiaries, today and tomorrow Your business relies on you and your key people. While equipment and other tangible assets can be relatively easily replaced, vital personnel cannot. Business protection provision helps shield your company against financial losses incurred by the serious illness or death of key staff. It protects against prolonged periods of reduced profits and against loans being recalled upon the death of a director. It also keeps ownership under control, for example when beneficiaries inherit shareholdings. Business protection agreements can, and often do, make the difference between survival and the decline of the business. At the very least they can ease the strain caused by seriously challenging, unforeseen events. What’s more, many schemes are very tax-efficient, making them an even more attractive investment. Business protection agreements include:

Shareholder Protection Agreements

This provides protection in life and death, ensuring remaining shareholders and partners can continue to run your company in the event of a death or serious illness of another. For example, in the event that a share of the company passes unfavorably into the hands of a deceased shareholder’s beneficiary, funds will be made available to recompense the family of the deceased or ill shareholder/partner for their share of the business. Often set up as a specialist business trust, they have the additional potential for tax savings. Key Person Insurance Most companies have one or more key employees - people whose knowledge and skills contribute significantly to the ongoing success of the business. In the event of their death or incapacity to work, replacing these skills can be a lengthy process and the negative impact on the business can be immense. Key person protection insures against the financial losses which death to long-term incapacity creates. Liability Protection: loans and borrowings Liability protection ensures that, in the event of the death or serious illness of a key person, the company’s outstanding borrowings are cleared. Lenders can be nervous and unsympathetic when a key person is absent: for example, director’s loans are normally instantly recalled on death. This causes additional strain or worse, at a time when the continuing success of the business is already compromised. Lenders will often make business loan protection a condition of the loan; we can arrange this for you very cost-effectively. Critical Illness Cover when a director or key employee becomes critically ill, the business is likely to continue to pay their salary and benefits while they are absent from the business - which of course can be a prolonged period. Additionally, the business may need to fund a locus to carry out some of their duties in the interim. Critical illness cover will alleviate the financial difficulties of this situation. Relevant Life Plan Many business owners are unaware of these tax-efficient plans, which provide death-in-service benefits to the families of one or several key employees. They are particularly useful for high-earning individuals or where there are too few employees to set up a group scheme. 4. Employee Benefits Packages: rewarding your staff Benefit packages play an important part in attracting and retaining the best staff, and a properly-communicated programme can help build trust, appreciation and engagement. They can also be tax-efficient ways to remunerate your employees – for them and for your company. We provide specialist advice and ongoing support to employers on implementing and running such schemes. We will help you frame your strategy to incorporate current and pending legislation, keeping you compliant and ahead of your competitors. Benefits we can advise on include:

We can also help you with group income protection, providing financial support to cover short or long-term illness. Understanding and buy-in It’s vital your employees understand the value of their benefits package, and that they have sufficient knowledge with which to make individual choices where appropriate. Rather than simply supplying documentation when staff join your company, we offer ongoing support to you and your employees, including:

You will have a dedicated consultant and the same administration team will handle all elements of your scheme. In addition, we can advise individual employees on financial planning outside of corporate schemes. 5. Retirement Planning What lifestyle do you envisage when you retire? When planning your retirement from your business, we believe it’s important to start with the end in mind: what you want to achieve, and when. That’s why we recommend a review of your pension/s – for example, amalgamating with your current provision any pensions you accumulated before going into business, simplifying the situation and enhancing the eventual outcome. Very often it’s possible to get your future pension provision working hard in your business now, presenting attractive and tax-efficient investment opportunities and access to funds you may not be able to get elsewhere, and at highly attractive rates. Specialist retirement planning options include (but are not limited to):

6. Succession Planning: What's next? What would you like to happen to your business when you retire? What would happen if you died while running it? It’s important to review your options and plan ahead, to cover all eventualities. Choosing the right options now can not only ensure the successful transfer of your business – to your beneficiaries, co-owners or a third party – but also present you with considerable tax efficiencies today and in the future. Whatever your thoughts, we won’t start work until you’ve agreed the terms, and the first consultation is at our expense. |

|